Table of Contents

- How To Calculate A Reserve Retirement

- A Quick Overview of How Active Duty and Reserve Retirement is Calculated

- More Details on Guard & Reserve Retirement Points

- Earning Annual Participation Points

- Earning Points For Service

- The Four Hour Rule

- Two-Hour Rule

- Doing the Math: Calculating Reserve Points

- What Is A Good Year?

- Retire Awaiting Pay, or Resign?

- Final Pay, High Three, or Blended Retirement System?

- Starting Retired Pay Before Age 60

- What is the Average Military Pension After 20 years?

- Want More Answers?

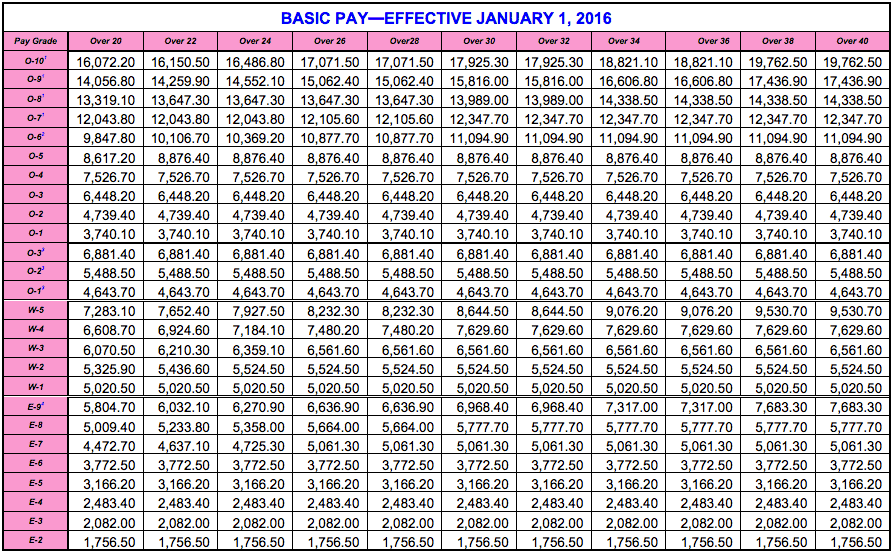

Note: Calculating retirement pay for the Guard and Reserves is slightly different from determining active duty retirement pay. This guide will show you how you can calculate your retirement pay. Note: This article uses data from the 2016 pay scale. However, the concepts are the same regardless of your pay grade or current pay scales. Simply plug in your current pay to these formulas to reach your anticipated Reserve retirement pay.

How To Calculate A Reserve Retirement

I recently answered a couple of questions on calculating the amount of a Reserve retirement for both Final Pay and High Three pay systems.

If you’re eligible for a Guard – Reserve retirement, then let me repeat the questions & answers so that you can confirm your math.

A Quick Overview of How Active Duty and Reserve Retirement is Calculated

Some of the processes are the same for calculating active duty and reserve retirement amounts. However, there are some notable differences.

In both instances, a retiree can use the Final Pay Plan or the High-36 Month Average Plan. Active duty retirement can also be calculated using the REDUX Plan.

- Final Pay is used for service members who first entered the military before September 8, 1980.

- The High 36 Plan is used for service members who first entered the military between September 8, 1980 and July 31, 1986.

- The REDUX Plan is available only to active duty members who entered service on or after August 1, 1986.

The biggest difference between active duty retirement and reserve retirement is when you can file. Active duty service members can file when their military career ends and they have accumulated 20 years of service. Technically, this means is someone enlists at age 18, they could start drawing retirement as early as age 38. By contrast, a reservist can only file for retirement when they turn 60, with a few exceptions, such as qualifying for early Guard/reserve retirement.

The other big difference is that active duty retirement is based on years of service while reservist retirement is based on an accumulation of points which are then converted to years of service.

In all cases, the Retired Pay Formula is determined by multiplying your retired pay base by a service percentage:

Retired Pay Base x Service Percent Multiplier = Gross Retired Pay

Gross retired pay is rounded down to the nearest dollar.

Next, each year of active duty service is worth 2.5% toward your service percent multiplier (2.0% for those participating in the Blended Retirement System).

So the longer you stay on active duty, the higher your retirement pay. For example, a retiree with 20 years of service would receive 50% of their base pay (20 years x 2.5%). A retiree would receive 75% of their gross pay after 30 years of service (30 years x 2.5%). Retirement maxes out at 75% of gross retired pay.

A retired reserve member converts points to active service equivalents by dividing those points by 360. For example, 7200 retirement points divided by 360 = 20 years of active duty service (2.5% x 20 years = 50%).

Until recently, the Final Pay Plan and High-36 Month Average Plan were the two primary non-disability retirement plans in effect for qualified reservists. However, reserve members also became eligible for the Blended Retirement System effective Jan. 1, 2018. The Blended Retirement System does not change how retirement points are calculated for members of the Reserves, with the exception of using a 2.0% multiplier.

For disability retirements, you would receive 2.5% for each year of service, or a disability percentage assigned by the service at the time you retire. In either case, the multiplier is limited to 75% by law. This article explains how disability compensation impacts your retirement pay.

More Details on Guard & Reserve Retirement Points

The following section goes into greater detail on earning retirement points in the Guard and Reserves. This is a good general overview. For a more in-depth article, check out this Guard and Reserve Points Guide. It goes into more detail and includes a podcast discussing the ins and outs of earning points in the Guard and Reserves.

When you’re in the Reserves or Guard, your time toward retirement is credited on two factors:

- the number of points you build up

- the number of “good years” you’ve completed

Each service is a little different in its point calculations. Points accumulate from both active duty and the Reserve/Guard system.

Earning Annual Participation Points

15 retirement points are awarded to Guard and Reserve members for each year of service. This includes times spent as a drilling participant or while serving in the Individual Ready Reserve (IRR).

A drilling participant is a member of a Reserve component who regularly serves a minimum of one weekend per month and approximately 14 days a year during annual training (AT). While their IRR counterparts, serve in inactive status after completion of active duty or electing to transfer into the component.

Thanks to Reservist and CFP Jeff Clark for researching the history of participation points. It’s discussed on page 164 of the 11th Quadrennial Review of Military Compensation. It’s the inset box which includes the text “Unfortunately, no documentation was available to explain the purpose or rationale for the 15 membership points. However…”

Earning Points For Service

You accumulate points for drill weekends, active duty periods, and under some special circumstances:

- completion of online or correspondence courses

- serving on funeral honors detail

- providing support to recruiting personnel

Each day of active duty counts as one point. Each drill counts as one point (a typical weekend has four drills), as do the days of active duty in the Reserve/Guard for training or mobilizations.

You’re also limited by the number of points you can get in a category — you can’t do 52 drill weekends in one year and get points for every one.

Of course, you can certainly be mobilized during a leap year and receive 366 points of active duty.

Here’s a minimum breakdown of points earned during a normal year:

- Annual Participation – 15

- Monthly Drills – 48 (12 months x 4 drills)

- Annual Training – 15

- Total points +/- 78

This article covers ways to earn more retirement points in the Guard and Reserves beyond the traditional “one weekend a month, two weeks a year“.

Note: It’s possible to get points for other purposes, but they’re limited. (For example, it was previously possible for officers commissioned from NROTC to receive points for the days they were on active duty for midshipman summer training, but they’ll need to supply the documentation. This niche benefit has since been revoked).

https://www.mynavyhr.navy.mil/Career-Management/Retirement/Officer-Retirements/Midshipman-FAQs/

The Four Hour Rule

During Inactive Duty Training (IDT), one point will be awarded for each 4-hour period of IDT performed.

A maximum of two points per calendar day applies to IDT Duty. Duty must be 8 hours in duration to receive two points per day.

Meetings (Seminars, Symposia, Professional Development). Per DoD Instruction 1215.07, members will only be allowed one point per day. Each training period must be a minimum of 4 hours in length.

Two-Hour Rule

Per DoDI Instruction 1215.07, the Funeral Honors requires a minimum of two hours of duty. Members receive one point for each day and the duty must be a minimum of 2 hours, including travel.

Doing the Math: Calculating Reserve Points

Reserve members can log a qualifying year for each year they earn at least 50 retirement points.

Inactive point credits are earned for inactive duty training, reserve membership, equivalent instruction, and correspondence courses.

The following point credits apply:

- Up to 60 inactive points for retirement years that ended before Sep. 23, 1996

- Up to 75 inactive points for retirement years ending on or after Sep. 23, 1996 and before Oct. 30, 2000.

- Up to 90 points in the retirement year that includes Oct. 30, 2000 and in any subsequent year of service.

Points from these sources may be added to points earned from active duty and active duty for training for a maximum total of 365 or 366 points per retirement year.

Points are credited as follows:

- One point for each day of active service (active duty or active duty for training).

- 15 points for each year of membership in a Reserve Component.

- One point for each unit training assembly.

- One point for each day in which a member is in a funeral honors duty status.

- Satisfactory completion of accredited correspondence courses at one point for each three credit hours earned.

Reserve members with 20 or more years to begin drawing retirement benefits before age 60 if they deploy for war or a national emergency. For every 90 consecutive days spent mobilized, members of the reserves will see their start date for annuities reduced by three months. However, because this was based on a law passed in 2008, it only applies for deployment time served after Jan. 28, 2008.

What Is A Good Year?

A “good year” ensures that you show up each year for a certain minimum amount of work. A good year is defined as one in which you earned a minimum of 50 points.

This can be accomplished if you show up for drills on at least 10 of the 12 months (or complete enough other assignments), then you’ve met the intent of a good year.

To be credited with a good year, you must earn a minimum of 50 points within 12 months (your retention year) and maintain your mobilization readiness (like completing the medical checklists).

This status is tracked in your service’s Reserve/Guard databases, and you may be issued occasional updates. Every year you can earn a certain number of points and get a “good year.” However, you’ll still have to verify that your service correctly credits you with that accomplishment.

You’re considered eligible for retirement when you’ve completed 20 “good years” of service. (But of course, you can usually choose to continue to serve.) If you have a combination of active duty and Reserve/Guard duty, then your active-duty service time counts toward the 20 good years.

There are also special circumstances (mainly medical) when you may be eligible to retire before reaching 20 good years. However, for purposes of this post, we’re going to assume that your retirement eligibility is based on the main requirement of 20 good years.

When you reach 20 good years, your service will eventually formally notify you that you’re eligible for retirement. (You may still have to finish other obligations like an enlistment, a minimum time in rank, or a set of orders.) When you complete those requirements (or have them waivered, or agree to retire at a lower rank), then you can apply for retirement.

The key to your retirement is that “notice of eligibility,” more commonly called “the 20-year letter.”

Retire Awaiting Pay, or Resign?

There are two ways to retire, and they require you to consider a certain amount of risk. The first option is to “retire awaiting pay”. Over 99.99% of Reserve/Guard retirees choose this option. When you retire awaiting pay you’re not required to perform any duties or maintain any readiness in the “gray area” between the time you retire and the start of your retired pay, but the risk of this option is that you could still be recalled to duty for a full mobilization.

A full mobilization requires the President and Congress to declare a war that’s bad enough to require the entire armed forces, and it’s more severe than the Presidential mobilization that was declared after 9/11.

Most Reserve/Guard retirees are willing to take this risk because the Department of Defense pays for it. If you retire awaiting pay then your seniority within your rank continues to accumulate, and when you reach your pension start date (generally age 60) then your retirement pay will be drawn at the active-duty pay table in effect that year. In other words, DoD covers you on both seniority and inflation.

You may also want to read the: Reserve Non-Regular Retirement Information Guide

If you’re not willing to accept the risk of a full mobilization, then the only way to completely avoid it is to resign. You’ll still receive your pension at your start date (generally age 60) but it’ll be at the seniority you had in that rank when you resigned– and in the pay scale in effect when you resigned.

This may not be much of a difference if you resign at age 59, but if you resign at age 37 then you’ll be facing over two decades of inflation erosion before your pension starts.

For the purposes of this post, we’re going to assume that you “retire awaiting pay”.

Final Pay, High Three, or Blended Retirement System?

The next question is whether you’re retiring under the pay base system of “Final Pay, “High Three”, or the Blended Retirement System (BRS). Both of them depend on the “Date of Initial Entry into Military Service” or “Date of Initial Entry into Uniformed Service”.

For most servicemembers, it’s considered the day that you first raised your hand, took the oath, and received an ID card. If your DIEMS/DIEUS date is before 8 September 1980 then you’re Final Pay. Otherwise, you’re “High Three”. If you joined the military with a DIEMS/DIEUS date after 31 December 2017, you’re in the BRS.

One loophole to this involves commissioned officers. If your commissioning source was a service academy, then your DIEMS date is the date you started at the service academy. However, when the services consolidated their pay systems in the 1990s, some members of the service academy classes of 1981-1984 were not properly credited with the correct DIEMS/DIEUS date. If you’re one of the few in this situation then make sure that your date is before 6 September 1980.

In addition, if you started at the service academy or signed an ROTC scholarship agreement before 31 December 2017, then when you commission you can opt into the Blended Retirement System.

Once you determine which retired pay base system you’re under, you’re ready to calculate your service percent multiplier.

The Service Percent Multiplier

If you had retired under the active-duty system with Final Pay or High Three, your multiplier would have been 2.5% per year of service. For 20 years of service, this is the “50% of base pay” that you’ve seen so much in the media.

Members who retire under the Blended Retirement System will use a 2.0% multiplier, which equates to 40% of your base pay at 20 years.

The Reserve/Guard retirement system calculates the multiplier from your total points.

Divide your grand total career point count by 360 (because your pay is based on 30-day months) and multiply by 2.5% (or 2.0%) to come up with your service multiplier.

For example, 2134 points / 360 * 2.5% = 14.82%. That’s your service percent multiplier, just as an active-duty retirement at 20 years would be 50%.

Pay Scale

Now you need your pay scale. If you “retired awaiting pay”, then your pay scale is on the pay table at the maximum longevity for that rank during the year that you turn age 60. (A few Reserve/Guard veterans may be eligible to begin receiving their pension earlier than age 60. We’ll get to that near the end of this post).

The problem with this calculation is that Reserve/Guard members who “retired awaiting pay” have to wait until they turn age 60 to know exactly what amounts are on that pay table. (If you’re only 38 years old when you retire, then you’d have to wait nearly 22 years to find out.)

The only suggestion I have for this situation is to assume that your pension will keep up with the current pay tables.

In specific terms, you’re assuming that military pay maintains pace with the Employment Cost Index. For a spreadsheet or a calculator, you could assume that military pay grows with the rate of inflation. This is not a very accurate assumption but it’s the best available for calculating future dollars.

A better assumption would be to convert your retirement income and expenses to today’s dollars and use today’s pay table. Take a look at the second page of the 2016 pay table.

If you retired as an O-6, there are pay longevity raises at 20 years of service, 22 years, 24 years, 26 years, and 30 years. It tops out at 30.

If you retired as an O-6 awaiting pay then you’d choose the maximum pay of that rank. In this case, an O-6>30 or $11,094.90/month.

If you retired as an O-5 then it’d be $8,876.40. At E-7 it’d be $5,061.30.

The Final Pay Pension

Whatever max pay you find for that rank, multiply it by the service percent multiplier and round it down to the nearest dollar.

That’s your monthly pension.

For an E-7 with 2134 points starting their pension in 2016 it’d be $5061.30 * .1482 = $750/month.

The High Three Pension

That’s a messier calculation.

Here’s what the Association of the U.S. Navy website says about High Three Reserve retirement in one of their articles (Note: the article is behind a membership login):

This system applies to anyone with a DIEMS of 8 September 1980 to present. Retired pay is calculated based on a figure derived from the average of the last 36 months of basic pay for the approved retired grade (highest grade satisfactorily held), and from the length of service (longevity) prior to reaching age 60. In other words, it is the basic pay in effect when you were ages 58, 59, and 60. The percentage of that figure (36-month average) you will receive is calculated by dividing your total points by 360 and multiplying that figure (equal to years and months) by 2.5 percent.

So you still start with your total points, divide by 360, and multiply by 2.5% to get the service percent multiplier.

Note that the multiplier is 2.0% for the Blended Retirement System.

But then the pay calculation is painful. You have to have 36 months of pay charts (the years you turn ages 60, age 59, age 58, and age 57). For each one, you’ll take the max pay at that rank (max longevity) and the number of months of that year. Then you’ll add them all together and divide by 36.

Here is an example:

Let’s say you turn age 60 in June 2012. You’d use six months (January-June) of pay for that rank at the max longevity in the 2012 pay table. For a High Three E-7, that’s $4815.90/month * 6.

Then you’d use 12 months of max pay for that rank in the 2011 pay table: $4740.00 * 12.

You’d add another 12 months of max pay for that rank in the 2010 pay table: $4674.60 * 12.

Finally, you’d add another six months of max pay for that rank in the 2009 pay table: $4521.00 * 6.

Now that you have the final 36 months of pay, you add all those numbers up and divide to get the final average monthly high-three pay:

($4815.90 * 6 + $4740.00 * 12 + $4674.60 * 12 + $4521.00 * 6) / 36 = $4694.35.

Note that it’s 97.5% of the Final Pay amount– only a 2.5% reduction.

That base pay number is multiplied by the service multiple to get the monthly pension amount.

$4694.35 * .1482 = $695/month.

Seems like a lot of work to shave 2.5% off your pension, but “high three” is commonly used in today’s defined-benefit pension systems to avoid the employee syndrome of “pension spiking”, a final year of work with exceptionally high pay. Congress and DoD just took advantage of a common civilian practice that doesn’t happen to be common to the military.

AUSN’s website doesn’t even have a calculator for the High Three Reserve retirement. They have a “Contact us” form that you fill out with the pertinent data, and then AUSN’s staff calculates the pension amount by hand.

By the way, if you join AUSN you’ll have access to all their website tools for Reserve planning, including the latest on when you’ll hear from your service and the pay center. You’ll be able to use their calculators and their guides on the Survivor Benefits Plan and their articles on retiree taxes. For a fee, AUSN will even review your record to determine how much you’ll be getting and what steps to take. I haven’t researched the question, but the other services should have similar Reserve/Guard advocacy organizations with similar support.

Starting Retired Pay Before Age 60

Some Reserve/Guard members may actually be eligible for a retirement earlier than age 60. The current legislation (passed in early 2008 and updated in 2015) reduces the age 60 retirement requirement by three months for every 90 consecutive days of mobilization during a fiscal year for war or national emergency.

In other words, a Reservist volunteering to deploy to the desert for a fiscal year would be eligible to start their Reserve pension at age 59.

A member of the National Guard who deploys with their unit for 24 months of the next five years (at least 90 days in the fiscal years) would be able to draw their pension at age 58. But this law only applies for deployment time served after Jan. 28, 2008.

Several amendments have been proposed to retroactively extend this benefit to September 11, 2001, but none of these modifications have yet been approved by Congress. There hasn’t been much support to this point, so don’t expect this will be made retroactive any time soon (if at all).

What is the Average Military Pension After 20 years?

This is a lot like asking how much a car costs. As an example, for retirement purposes, 20 years is the minimum qualifying level, but many service members serve additional years. The Department of Defense uses a multi-step formula to compute retirement benefits pay, so there is no single accurate answer when it comes what the average reserve retirement pay is.

The only way to address this question is to consider your individual circumstances. You need to consider these factors as a starting point:

- How many years did you serve both active duty and as a reserve member?

- Which years did you serve?

- What was your rank at retirement?

- Are there questions related to how a Social Security benefit and a federal retirement benefit interact with each other?

- What were your earnings that have an impact on how your retirement pay is calculated?

- Which formula applies to you?

- Does military disability enter into the picture?

- How about Extraordinary Heroism Pay?

Want More Answers?

If you have questions about either active duty or reserve member retirement plan benefits, contact the appropriate Defense Finance and Accounting Service (DFAS) office:

- Air Force, Army, Marine Corps, Navy, Space Force active duty or Reserve, call 1-888-332-7411.

- Retiree, survivor, or beneficiary, call 1-800-321-1080.

Military Guide to Financial Independence

This book provides servicemembers, veterans, and their families with a critical roadmap for becoming financially independent. Topics include:

- Military pension

- TSP

- Tricare Health System

- & More

Comments:

About the comments on this site:

These responses are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser’s responsibility to ensure all posts and/or questions are answered.

S.P.Denham says

Hello I am due to start receiving my reserve pay which is estimated to be 1300 a month. However I currently receive a 30% disability payment of $650 monthly. How will that disability affect how much I get from my reserve pay. An estimate would be nice..

Ryan Guina says

S.P.,

I don’t have a lot to go on by your comment. If you are a retiree, your military retirement pay will be offset by your VA disability compensation. You can read more about how VA disability impacts retirement pay in this article.

If you are currently serving, I encourage you to read the following two articles to get a better idea of how a VA disability rating impacts your ability to serve in the Guard or Reserves, and how to determine whether to waive military or VA compensation for the days you served in both statuses.

Regarding serving with a VA disability rating: you can only earn one type of pay on any given day. You can’t earn VA disability compensation on the same day you earn military compensation. Because there is no way for the VA to track this in real-time, you will receive a form each year outlining the days that you received compensation for both payments. You will then need to choose one to waive. These benefits are pro-rated based on the monthly compensation rate. In almost every case, it is best to waive the VA disability compensation. If you choose to do so, the VA will withhold a portion of future payments until you have repaid the debt. The above article outlines the details.

Best wishes!

Dean O says

Aloha Doug,

Is there a difference between your TAFMS and PCARS when retiring? An Air National Guardsmen had 4 yrs Active duty, spent the next yrs as traditional Guardsmen then got an AGR IN 2023.

At this point he accumulated 12 yrs of TAFMS and around 5400 points (15 yrs). Say he works 8 more years (he’ll be 55yrs old) has 20 yrs TAFMS and 23 yrs of points. Question is what’s his retirement at TAFMS or PCARS?

Mahalo

Dean O

Ryan Guina says

Dean, I can’t speak for Doug, but I’ll answer to the best of my ability.Your TAFMS is your Total Active Federal Military Service. This only counts your active duty time. Your PCARS should inclue all of your points, including TAFMS and inactive points. You need 20 years worth of TAFMS to qualify for active duty retirement benefits. You just need 20 good years to qualify for Guard or Reserve retirement benefits.

In your example, this person can retire with active duty benefits once he has 20 years of TAFMS. But since he will have 23 years worth of points, his retirement would be based on 23 years worth of points. And since it would be the equivalent of an active duty retirement, it would start the month after he retires, instead of him having to wait until age 60.

I hope this helps!

Dean O says

Mahalo Ryan.

It clears up a lot of confusion we have between the Air National Guard (AGR’s, Technicians, and Week End Warriors) and Active Duty Air Force and their retirements.

Joe S says

Hi Doug.

I’m an Army civil service employee with 25 years in GS with 10 years ADAF time (1982-92) that I could buy back for a total of 35 years. I’m expecting to pay $8,000-$10,000 for the buyback.

Because of the 10 years ADAF and 9 good years in the MI ANG (2002-2010), I am one year shy of an ANG retirement. I had to separate at 19 due to family issues, and since I’m 59, that one-year door will close in June 2024, but I’m still trying to get back in to complete at least one year. If successful at completing that one year, I would be eligible for an ANG retirement. I have around 4,700 points. Where can I find a calculator (or someone who can calculate) that would give me a ballpark figure based on my unique circumstances?

Thank you.

Ryan Guina says

Joe, I can’t speak for Doug, but I can walk you through this. First, I wish you the best of luck in returning to the military to earn a final year and qualify for retirement. Next, you have a lot to be proud of. Definitely buy back your military service time for your civil service pension. It will be well worth it!

Regarding estimating your military retirement benefits, if you can get back in – you have the information in this article. divide 4,700 points by 360, and you get 13.05 years. To make things easier, use 13 as your time in service multiplier, which gives you 32.5%. Then multiply 32.5% by the average of your High-36 pay. I don’t know your rank, so I can’t do that for you. But you can easily do it. You will need to take the base pay for the highest held rank for the last three years and average it. Then multiply that by 32.5%. That should provide you with a rough estimate. If you get back in the service, your personnel or human resources office can run an official estimate for you. But this can serve as a back of the envelope calculation until you need a more accurate estimate. Best wishes!

SSG.RET HUBERT BALLARD says

IM TRYING TOFIND OUT DO I GET ANY POINTS FOR BEING IN THE RETIRED RESERVES ADD TO MY POINT I ALREADY HAVE I WENT INTO THE RETIRED RESERVES IN2007,MY 60 BIRTHDAY WII BE NEXT YEAR

Ryan Guina says

SSG Ret Ballard, no, you will not generally be able to add points to your retirement total once you have retired. You can contact your branch of service’s Human Resources or Personnel office for more information on your points total. You should be able to contact DFAS to obtain an estimate for your monthly retirement pay once you become eligible. Just be aware that there will be one more cost of living increase between now and next year. Best wishes!

Mike L. says

Hello Doug,

I am extremely grateful for this trend and the amount of information it has to offer. I have looked all over the internet for help, and the information captured here is by far the most informative I have been able to find.

Here is my story: I am an Army E-9 with 27.5 years of good years. Out of these years, as of today (22-MAR-23) I have 19.3 years (6978 points) of active service and the remaining 8.2 years (638 points) as a drilling reservists (TPU).

I am currently on active duty orders assigned to a Soldier Recovery Unit (SRU). I was mobilized with my unit on December of 2020 and while mobilized I was injured. Instead of separating at the end of my tour, I was transferred to the SRU where I continue to be in active duty orders. While in the SRU, I was submitted for a separation board (MEB), where I was found unfit for duty. The informal PEB came back with a DoD rating of 30% and VA rating of 80% and PDRL. Nevertheless, I was already rated at 100% P&T for my previous AD.

I requested a formal PEB and it currently scheduled for the end of July 2023. By the time I go through the formal board and get my no later than date (separation/retirement date) I will have over 7200 points of active duty and nearly 7900 points total.

My questions are: Would I be able to retire from active duty since I have over 7200 point? Would I be allowed to receive concurrent retirement of DoD and VA pay? What is the benefit of the 30% of DoD rating on my retirement, if any?

I truly appreciate your insight on this. I can’t seem to get information on my situation.

V/R, Army CSM

Ryan Guina says

Mike, I can’t speak for Doug, but my understanding is that you should be able to retire from active duty once you reach 20 years of Total Active Federal Military Service (TAFMS). Once you have those 20 years of active duty service, your 638 Reserve points should be added to your retirement total (638 points / 360 days = 1.77 years added to your retirement multiplier, or roughly 4.4%, bringing you up to about 54.4% of your high-36 months).

You should be eligible for concurrent receipt if you receive a “normal” military retirement, not a medical one.

There is no real financial benefit to having the 30% military disability rating. Your military retirement pay will be worth more than the military medical retirement pay would be at 30%. And your VA disability rating is separate from your military retirement pay.

I hope this points you in the right direction, and I wish you the best of health!

Matt K says

Hi Doug – first and foremost, THANK YOU! I’ve read almost every word on this page and it is the single best source for this topic I’ve found to date. I appreciate all of the time you take to respond to each question.

I believe my situation is unique, as I do not see it addressed here.

This is about the double-dip (collecting both a military pension and FERS pension)!

I am a guardsman on track to be eligible for a 20 year active duty retirement – not all points are created equal, but we’ll just say 7200 points. I am also a GS employee, completely separate from my duty as a guardsman – so, not a technician. Next year I’m eligible to receive a 20 year active duty pension. Can I buy back all that time at my GS job while still receiving immediate military pension benefits?

I ask this because I’ll be retired out of the reserve/guard (10 U.S. Code Chapter 1223) but the pension is active duty, in nature, because I’m immediately receiving a check. Since I retired as a reservist, is it still a reserve retirement? Or as soon as we request our check early (20 yr AD retirement / 7200 points), does our retirement status switch to “active duty?”

Thank you so much!

Doug Nordman says

You’re welcome, Matt! I’m paying it forward, and I’m glad it’s helping.

If you’re earning an active-duty military pension, then that will starts as soon as you retire from your final set of orders. The Dept of Defense will do that regardless of your civil-service career.

If you’re earning that active-duty pension from Chapter 71 of Title 10 (instead of a Reserve pension from Chapter 1223) then it’s considered a regular pension and not a Reserve (non-regular) pension. Even if you achieved this pension through declaring sanctuary, it’s still an active-duty pension.

However the federal laws (passed in the 1960s) about dual compensation will limit your ability to buy your military service credit deposit with your FERS pension. OPM enforces the dual-compensation laws.

https://the-military-guide.com/earning-military-pension-civil-service-pension/

The only waivers in that situation are for a military disability pension, or for a Reserve pension, or if you give up your active-duty pension. However you can still buy a portion of your military service credit deposit to adjust your Service Computation Date, your Reduction In Force date, and your annual leave accrual rate multiple:

http://gubmints.com/2013/04/15/military-service-credit-deposit-retired-from-active-duty/

In very general terms, it only makes sense to give up your active-duty pension if you retired at a relatively junior enlisted rank and reached a very senior civil-service rank.

Matt K says

Thanks Doug!

2 more curiosities:

Since I’ve done over 10 years of active duty as a reservist (mix of RPA, MPA, and AGR status), that reduces my retirement age to 50, right? (AGR counts toward reducing retirement age, doesn’t it?)

Lets say I’ve officially reduced my retirement age from 60 to 50. If I start collecting a pension at 50, would that be considered a reserve retirement and therefore I could buy all that time back in a civil service position?

Thank you again so much for your time and patience!

Doug Nordman says

Matt, a Reserve early retirement is completely separate from an active-duty pension, and a Reserve early retirement depends on the nature of your active-duty orders. AGR orders do not necessarily qualify. You’d have to be mobilized to a combat zone after 28 January 2008 for at least 90 days in a fiscal year. In 2013 the law was amended to add mobilizations for natural disasters, again for at least 90 days. You can read all the details at this post:

https://themilitarywallet.com/national-guard-and-reserve-early-retirement-age/

Again, if you serve for 20 years of active duty and retire (at any age) on an active-duty pension, then it’s not part of the Reserve retirement system and it has nothing to do with Reserve early retirement benefits.

matt k says

Thanks so much!

JOHN PARCELL says

Hello- I spent 11 years in USMC being discharged after Gulf War number one. I reentered PA Army National Guard in2001, retired in 2013. I have approximately 5800 points total. and I filed my retirement application in early 2021, a problem arose and asked for assistance from PA ARMY GUARD admin personnel. It was resubmitted, by PAANG , in 11 -2021, and HRC says that they got it to process in 12-201 and thats the date it will be processed from at this time, even though my early retirement date was 10-2021 (I spent several tours since 9-11 01 in Bosnia and Iraq) . They stated in an email reply that my application will be process per my DOB or Early Age drop date) but no firm date can be given for processing. . Can you help me understand this system? TY

Doug Nordman says

John, you’ll want to check all of your combat deployment dates since 28 January 2008 against the early-retirement requirements listed in this post:

https://themilitarywallet.com/national-guard-and-reserve-early-retirement-age/

Depending on the dates you deployed, their duration, and their timing around the fiscal year, you may be eligible to start your pension three months earlier for every 90 days in the combat zone. Earlier versions of the law (which applied to you but were amended in FY 15 after you retired awaiting pay) required all 90-day periods to be served in the same fiscal year.

HRC and all of the other services have to manually review and calculate the mobilization orders, locations, and dates in order to validate the early-retirement eligibility for each 90-day period. (There’s no automated system to assist in this.) In addition, all of the DoD federal civil service staffs have been backlogged in processing these requests due to the pandemic remote-work requirements, a wave of civil-service retirements, and the slow hiring/training of new employees.

I can’t predict when HRC will approve your retirement application and send it over to DFAS, but DFAS will tell you (in their letter) that they’ll start your pension deposits within 30-45 days after they receive the ANG approval. It’s possible that you may see a status update in your MyPay account, although that depends on the timing of DFAS running the payroll/pension process around the 20th of the month. Your first deposit (at the end of the month) will be paid retroactive to the early-retirement date that you’re eligible to start your pension. Subsequent deposits will be the regular amount of your pension.

When your retirement application is approved, at your 60th birthday you can update your Tricare enrollment in DEERS. (Although you’re receiving an early pension, Tricare still starts at age 60.) You might need several weeks of lead time to get an appointment at a RAPIDS office, but your Tricare benefits will be retroactive to your 60th birthday.

Maria Teresa Limbo says

I was in the Army Reserves and I retired active duty under Title 10, 12686 Sanctuary. I accrued a total of 7797 points which 20 years active duty and 1032 inactive duty points combined. I have performed 20 years active duty and I still have 1032 inactive duty points. Do you know what happens to the inactive duty points when you retires active duty? Do you loose it? Do you know what regulation states that you forfeit your inactive duty points when you retire active duty? Please let me know. I called the Army HRC and I was told by the customer service that I forfeit it but could not show me the regulation.

Doug Nordman says

Maria, it’s a shame that HRC couldn’t make the effort to provide a regulation. I’m not familiar with their claim that you forfeit any of your points.

My understanding of the process comes from the Financial Management Regulation (DoD 7000.14-R) Volume 7B Chapter 3:

https://comptroller.defense.gov/Portals/45/documents/fmr/current/07b/07b_03.pdf

Your 1032 additional points are divided into 360 and added to your 20 years for a total of 22.87 years of service.

I’d recommend checking this with your command’s financial personnel (if they’re familiar with sanctuary), or HRC’s sanctuary office, or a JAG at your base legal service office. If you haven’t already talked to HRC’s sanctuary office, you can find them at:

https://www.hrc.army.mil/content/Enlisted%20Sanctuary%20Program

[email protected] or by phone at 502-613-5962.

As a side question, I’m not sure of your math for 1032 points of other than active duty from your 7797 point count. Presumably you’re working from HRC’s audit of your sanctuary request.

Duane Eldridge says

Why can’t I find any mention of using the max pay for your paygrade when you turn 60 in the calculation for your retired pay when I am looking on an official Navy website such as MYNAVYHR? I always see that they have you enter the pay for the years of service you had in your pay grade at retirement. I am a retired CWO3 gray area reservist turning 60 this June. I fall under the Final Pay category of retirees.

John says

I’m not sure, but if you are a gray area reservist it is the total time from your PEBD until you start drawing retired pay. All that time in between counts for longevity. For most people, this maxes them out. I guess in some situations it may not. Maybe if you didn’t start your career til very late and/or had broken service.

Doug Nordman says

Congratulations on your pending pension, Duane!

As John says, the federal law for retired awaiting pay is “… as though the member had been on active duty the entire time” during gray area. For most ranks and ages it’s the maximum longevity pay in that rank. However those who’ve joined the Reserves in their 30s (or had significant broken service) might not reach the maximum pay for their rank by age 60.

I’m not familiar with the website calculator you mention, but it probably does the math for your years of service and your age to forecast your pension at age 60. For a more relevant number you could calculate your pension in today’s dollars with today’s pay tables (using the longevity you’d have at age 60) and compare that directly to your current expenses. By using today’s dollars, you don’t have to account for inflation.

Richard Gray says

Hi Doug,

Great article and I found it helpful, but I have some questions that I am having trouble finding answers to. I retired 1/1/2020 from the Navy Reserve as an 06 with 20 credible years. I fall under the High 3 for retirement purposes. I turn 60 in October of 2021. If I follow all the formulas as I understand them, it appears that my retirement pay is more than what I was making per month as an active Reservist. I find that hard to believe.

I retired with 2421 points. When divided by 360, that gave me a value of 6.725 and that was multiplied by 2.5. My percentage multiplier came out to 16.87 or .1687. In terms of rough estimates I looked at the pay tables for 2017-2019. 2017 I was an 06 at 18 years and 2018-2019 I was 06 at 20 years. In adding all the numbers and dividing by 36, I came up with 10,149. I then took that number and multiplied it by .1687. That gave me a value of 1712.14.

I find it hard to believe that my retirement pay would be $1712.14 a month. My last drill pay was $1408 in Dec of 2019. What am I missing here? I was expecting my retirement pay to be in the range of 600 a month. I do not believe for a second that it would be the full amount and more than I made as an active Reservist. Thanks so much for any help.

John says

Doug, it’s certainly possible. I was an E-5 when drilling and probably only got like $400 for a drill weekend. But now retired, (I was bumped up to E-6 upon retirement), my gross retired pay is about $1200. Of course I had over 4000 points (10+ years I was AD).

Keith McCullar says

Richard,

Your calculations aren’t correct. You improperly calculated your High 3. That number isn’t based on O6 pay at the end of your career. It’s based on O6 pay for the 36 months prior to the date you begin drawing retirement pay. Typically your 60th birthday but there are exceptions. Plus you are entirely at 06 over 20 because that’s what you were when your career ended. So you sold yourself short. Your retirement pay will be more than you calculated.

Look at it this way: your points are about one-third what an active duty retiree would have after 20 years. Their pay would be half of what they were making (not including allowances) or 15 days worth. So you will be getting paid about five days worth which is more than you got paid for a four-days-of-pay drill weekend.

Congratulations on your retirement. Go forth and do great things.

Keith McCullar

CPT (Ret.)

Doug Nordman says

Richard, as John & Keith point out above, it’s certainly possible.

Let me call your attention to a couple of critical details in the post.

First, the pension is calculated using the pay tables in effect when you start it. In your case (at age 60), it’s the High Three average of the 2021, 2020, 2019, and 2018 pay tables.

Second, it’s at the longevity as if you’d been on active duty the entire time up until you start your pension. This means that your years of service continue to accrue.

The result is that while you’re awaiting pay (gray area) your pension is boosted by annual pay raises (tied to the Employer Cost Index) and longevity pay raises (years of service in the pay tables). In general, your eventual pension more than keeps up with inflation during the gray-area years.

The tradeoff for DoD’s pension generosity is that “retired awaiting pay” Reservists are subject to involuntary recall for a total force mobilization, which last happened during WWII.

If you had a December 2019 drill weekend of $1408.44 then you were indeed an O-6 over 20 years.

https://www.dfas.mil/Portals/98/MilPayTable2019_3.pdf

Since you were an O-6>20 in 2018-19 then I’ll assume that in January 2020 you became an O-6>22. You can correct the numbers below for your actual date that you went O-6>22.

In October 2021 your High Three average becomes:

https://www.dfas.mil/MilitaryMembers/payentitlements/Pay-Tables/PayTableArchives/

2020 and nine months of 2021 as an O-6>22,

2019 as an O-6>20, and

2018 for three months as an O-6>20.

Working backwards from the 2021 pay tables to 2018, your High Three pay average is:

[(9 x $11,512.80) + (12 x $11,177.40) + (12 x $10,563.30) + (3 x $10,295.70)] / 36 = $10,983.08

Your High Three pension would be:

$10,983.08 x (2421 / 360) x .025 = $1846/month.

By the way, BUPERS N9 is backlogged due to civil-service retirements and pandemic labor shortages. You should consider applying for your October 2021 pension now. See the section “Applying for Retirement with Pay” at:

https://www.public.navy.mil/bupers-npc/career/reservepersonnelmgmt/ReserveRetirements/Pages/default.aspx

John says

Yes. The unfortunate and unfair aspect of all this is after you start getting your pension, all that work and effort and service & time you did, to earn and calculate your Service Percent Multiplier means NOTHING anymore. From then on your increases are tied to COLA’s, no longer to your EARNED percentage of your paygrade’s & time’s actual Active Duty Pay. That should be changed.

Jones Donald G (Don) says

I found a form DD Form 2586 Verification of Military Experience and Training NGR and AR but does not include active duty in AF. First service December 1966 and 19 years. Yep I’m 73 ! Is there any chance of getting anything ? If so where do I go to find out? Thank you for all your hard work.

Dean Swann says

Doug, your article was super helpful. I am so thankful for your help, I went on Amazon and bought your book!

Doug Nordman says

Congratulations on your impending pension, Dave!

You’re under the Final Pay pension system (entered service before 8 September 1980), so you can try this calculator:

https://militarypay.defense.gov/Calculators/Final-Pay-Calculator/

and choose the Reserve Component options.

The factors in the Final Pay calculator are:

Monthly pension = [points / 360] x 2.5% x base pay.

Your base pay will be from the 2022 pay tables, which haven’t been published yet. (It’s reasonable to project a 1.5% pay raise.) Your pay will also be at the longevity for your rank as though you’d been on active duty the entire time that you were retired awaiting pay, which in your case is the >40 column:

https://www.dfas.mil/MilitaryMembers/payentitlements/Pay-Tables/

You can read through the retirement application instructions here:

https://www.public.navy.mil/bupers-npc/career/reservepersonnelmgmt/ReserveRetirements/Pages/default.aspx

“Applying for Retirement with Pay

1. Notification is forwarded in advance to advise you how to submit an application for retired pay at age 60. If you have not received notification four months prior to your 60th birthday, please contact PERS-912 by calling 1-833-330-6622.”

However BUPERS has been shorthanded on processing pension requests, and you may want to apply as early as June (nine months in advance).

Your Tricare options are essentially Tricare Prime or Tricare Standard, unless you’re in a rural area of the U.S. or living overseas. You can compare the various programs (and their co-pays and prescription expenses) here:

https://www.tricare.mil/Costs/Compare

We’ve been happy with Tricare Prime (especially raising an accident-prone teen) but Tricare Standard can work well if you’re not seeing a lot of doctors (and making a lot of copays).

Doug Nordman says

Don, that form lists your military training and experience. It doesn’t verify that you have 20 good years of Reserve or Guard service and has no impact on military pensions or veteran’s benefits.

I think you’re asking whether you qualify for a Reserve pension. You can learn more about that by contacting your final service (the Army Reserve?) at the Human Resources Command (https://hrc.army.mil/) to request a copy of your Notice Of Eligibility letter.

You can also discuss whether your point-count records with them include your previous active duty.

If there’s an error in your records then you could try to update the HRC database with your active-duty service, and see whether that meets the requirements for a NOE.

If you’re asking about veteran’s benefits or a VA disability claim, that’s handled by a Veteran Service Officer. You can find them through local chapters of the American Legion, the DAV, the VFW, or even MOAA. You can find them in your area through the VA’s website:

https://www.va.gov/vso/

And you can also contact your state’s office of Veteran Affairs.

Doug Nordman says

Thanks, Dean, I appreciate the support!

John says

All seems right on. I stopped drilling in Oct 1998 (had a little over 20 years, about 10 active and 10 reserves). I went to the Ready Reserve (gray area). Filed for retired pay in July 2019, 2 months before my 60th birthday. Got first check in Nov 2019 and another catch-up pay in Jan 2020. But what I just found out about, and really irks me, and we need to get congress to change is how your pay is “reduced” in years following retirement. My Service Percent Multiplier came to 31.88% and initially I got that percentage of an E-6 with over 42 years. But now, instead of still getting that same percentage of an E-6’s pay for 2021, I only get a lousy minuscule COLA put on that. So the value of my retirement has just been diminished. This is made even worse by the fact I chose Tricare Select and was fine for 2020. But now for 2021 I have to pay $25 a month to cover my wife & I. So actually, my net retired pay has gone down $10 a month. Up $15 for the COLA, but down $25 for the “enrollment fee”. If I were still getting 31.88% of an E-6 with over 42, the increase would have offset the new fee. How can we get this changed for all retirees?

Megumi Voight says

Hi Doug!

Holy cow, thank you for all of the time you’ve taken to write this article and respond to all of us regarding our individual cases. Another one for you ;). I’ve been trying to calculate what my retirement pay will be as I do some financial planning for the future.

– Commissioned in May 2012 (at age 21)

– Active duty for 5.5 years (until November 2017)

– No break in service before joining the USAFR as a TR

– I plan to stay in a TR/IMA status in the USAFR for 20 years (until 2032)

– Playing it safe for financial planning, I estimate having the minimum number of points to qualify for a good year for the 14.5 years in the TR/IMA role (so I think that’s ~50 points/year?)

– Selected to stay enrolled in High-3 rather than BRS.

My main questions given the situation above are:

– If I retired as an O4, what would my monthly retirement be? As an O5?

– Because I hit my 20 years of service at Age 41, but I won’t be eligible to receive benefits until 60, what happens since I won’t have paystubs from Ages 58, 59, 60?

I hope that all made sense haha!

Thank you!

Megumi

Margaret Dirsa-Dubois says

How can I talk with a real person who can help me? I live in Florida. I joined active army in 1978 and spent a total of 12 years of active duty and another 12 years of Army National Guard with a total of more than 25 years! And now I get a deposit in my account that seems Very Low! I have nothing in writing in response explaining how this amount was made and I don’t have anyone to ask. Who can I talk to? Yeah, I sent an email to DFAS and got an email saying they have my email — but no actual answer. I don’t live near any fort or base. Please point me in the right direction.

Joseph says

Hello, short of calling the AFPC, I’m trying to figure out if I will have to repay my Voluntary Separation Pay (I was on AD for 10 years and will be completing the second 10 years as a reservist) to be eligible for the pension. I’ve heard you have to repay it, but can’t find the source document, and am also wondering if it’s the pretax or the post tax VSP amount. Thanks in advance!!

Joe

Cori Wilkerson says

I am in the COARNG now and just hit my 20 years service (10 years was on Active Duty). I have my points statement and trying to get my unit to figure out dates eligible for the qualified service to reduce from age 60yo. They are only counting one 6-month Title 10 orders from the age of 60, so 59.5 years old to retire. If I was on active duty for 2 deployments after the 29JAN08 date that was approved—— Does my AD deployments count as qualified service to subtract from the age 60 retirement date (this is 26 months worth)? Or just the times I was called to AD from being in the Reserve/Guard (only 15 other months)?

Todd Mingin says

Doug,

Thank you for doing this for all of these years. I do wish I would have found you sooner but it’s a blessing all your hard work exists at all. When I first enlisted in the active duty AF, it was for at least 20. Things changed over that initial six years and now I’m at my 20 year mark in two weeks. I was planning on staying in longer but things have become much crazier for me. I’m replying with a question concerning the 10 year rule, retirement, and retention of my commission.

I’m a 40yo Air Guardsman, 6 active, 14 guard, and I was commissioned at my 17th year to O-3 for my medical education as a physician into a program under the medical service corps. To move into the full medical corps as a doc, a re-recruitment process must take place. It’s taken over three years and it may need to be re-accomplished again due to lapse in shelf-life of the paperwork. Ultimately this process has been pretty frustrating leading me to consider retirement vs. IRR vs. who knows what else it out there. If it is no longer fun, then it might be time for a change is what I was told a long time ago and have seen it repeated in your comments.

Concerning retirement, if I am unable to retain my commissioned rank my pension drops significantly upon reverting back to E-6. Where can I find out about the 10 year rule and if or how it applies to me? Does reverting to an inactive ready reserve status continue to accrue this time if this does apply to me? How difficult is it to revert back to drilling status from IRR?

Sonita Wong says

Hello, I was in the army reserve for eight years, and my unit disbanded years ago…I do not have my army reserve points statement in my records… How do I make or find the people to create and calculate a points statement record???There is no personal from my old unit to contact…Thank You…

Tom says

Great article Sir. My question: Is PEBD used during calculation of my retirement pay ? I had a break in service between active duty and Reserve and PEBD date is incorrect. However, everyone has told me that it is very difficult to change it requiring enormous load of paperwork and it is not worth the effort. Should I try to correct it or should I leave it alone if PEBD will not be used to calculate my retirement ? Thank you.

Gary L Taylor says

I had always “heard” that you needed to hold a rank for 6 months to retire at that rank. I requested an extension of my MRD for two years and they gave me one, forcing my retirement at 61 and holding my 06 rank for 1.5 years. I had assumed since I was forced out by MRD (not my choice or voluntarily retire) my pay would be at the 06 rate, but instead they blended it to 1/2 05 and 1/2 06. It seems if forced out involuntarily due to MRD they should base your pay on the new rank since it wasn’t the soldier’s choice.

Francis says

Doug, if I hit 20 good years at age 43, can I still be affiliated with the Reserves(pay or non-pay)? If so, this would be an excellent option to continue with Tricare Reserve Select for at least a few more years. Thanks.

Doug Nordman says

Zach, I’m pretty sure that does not count. It’s only for mobilizations to combat zones and (much later) national emergencies. It’s actually three months of earlier retirement for every 90 days deployed in those situations, and in most cases the 90-day period had to be within a fiscal year.

You can read the full discussion of the qualifying criteria at this post from my friend (and National Guard servicemember) Ryan Guina:

https://themilitarywallet.com/national-guard-and-reserve-early-retirement-age/

Zach says

Great article and I really enjoyed reading the comments and questions of others. I have 8.5 years of active service and have now served as a reservist for 3 years. Regarding the early reserve retirement date (subtracting 90 days at a time from age 60) I was hoping to get some clarification. I know you have to be in a reserve status called to active duty for the reduction to occur. Considering I was an ROTC cadet who selected active duty, does that count as being called to active duty and apply for the reduced retirement age?

Doug Nordman says

Mike, those are great questions, and I’m pretty sure that federal law (Title 10 U.S. Code section 1370) takes precedence over AR 135-180. However it looks like the Retirement Services section misread Table 4-2 on page 10 of AR 135-180. You can confirm that with a JAG or with a civilian lawyer who has military experience.

The relevant part of federal law is 1370(d)(3)(A):

https://www.law.cornell.edu/uscode/text/10/1370

“(A) In order to be credited with satisfactory service in an officer grade above major or lieutenant commander, a person covered by paragraph (1) must have served satisfactorily in that grade (as determined by the Secretary of the military department concerned) as a reserve commissioned officer in an active status, or in a retired status on active duty, for not less than three years.”

Paragraphs (B) through (F) cover some exceptions to that three years which apply to very few people. They’re essentially for situations beyond your control which prevent you from serving three years, or when you’re an O-5 select (still awaiting Congress’ approval for promotion) serving in an O-5 billet.

The part which I’m frequently asked about is paragraph 1370(d)(5)(A). It authorizes the Guard to waive that three-year requirement to two years:

“(A) The Secretary of Defense may authorize the Secretary of a military department to reduce the 3-year period required by paragraph (3)(A) to a period not less than two years.”

You have to request the waiver, they have to approve it, and two years is a hard minimum. Two years is usually approved during drawdowns when someone’s already available to take your billet.

Table 4-2 of AR 135-180 appears to match federal law with the “Voluntary separation” column for the “Officer: O5 and above” row requiring three years. The six months would only apply if you were being involuntarily retired (1370(d)(3)(B) through (F)).

From the vocabulary used during your conversation with the Retirement Services section, it’s possible that they misunderstood your question. “High Three” is a pension calculation, not a time in grade. If your Date of Initial Entry into Military Service (the date you received your very first military ID) is before 8 September 1980 then your pension is calculated using the Final Pay system. That’s pretty rare these days, and us remaining Final Pay dinosaurs who are still in uniform are either admirals/generals or Reserve/Guard members with very long breaks in service. Let me know if you have a DIEMS before that date, even for the Delayed Entry Program or by attending a service academy.

Otherwise if your DIEMS is after 7 September 1980 then your pension is High Three, calculated from the average of the highest 36 months of pay received during your career. (That’s completely separate requirement from three years’ time in grade.) For a Reserve pension you’d retire as an O-5 if you met the Title 10 U.S. Code section 1370 requirements, and then the High Three calculation would determine the pay factor in your pension. If you did not meet those time-in-grade requirements (or at least get a waiver to two years) then you’d be retired as an O-4.

Those DIEMS dates and High Three calculations are in paragraph 4-6 of AR 135-180 and also in federal law.

I’ve been crunching pension numbers for nearly 20 years, and I have no idea where that point-value system came from. (It’s certainly not in federal law or on DoD’s website.) Every time I get that question it causes confusion– even if the Guard tables are up to date. I find it far easier to manually calculate the High Three average.

As mentioned in the post above, once you have your Notice Of Eligibility letter then there are two ways to receive a pension from the Reserves or Guard. One way is “retired awaiting pay”, which almost everyone chooses. (The other option is “discharge” or “separation”, which I’ve only seen twice.) When you apply for “retired awaiting pay” then your High Three pension is calculated from the pay tables in effect at the time you start your pension. (That’s usually age 60, or possibly three months earlier for every 90 days mobilized to a combat zone or for a national emergency.) That’s because during the grey-area years of “retired awaiting pay” you’re technically subject to activation for a total force mobilization (which last happened in WWII) and you’re considered to be serving (for the longevity column in the pay tables) as though you were on active duty right up to the day your pension starts.

This means that you have to serve three years’ time in grade to retire at the rank of O-5 (waiverable down to two years) but you do not have to worry about MRD. You’re simply continued in your “retired awaiting pay” status until you reach age 60. You’re given all of the increases in the pay tables because your pension will be calculated from the pay tables in effect in 2034– and at the O-5 longevity as if you’ve been on active duty the entire time.

Mike Vaughn says

Doug,

Good morning. Outstanding article and feedback. I am similar to one of the comments above. I am a Traditional National Guardsman (i.e. one weekend a month and two weeks a year) who will receive a non-regular retirement. I was promoted to LTC (O5) in July 2018 and can’t seem to get a definitive answer concerning the 3 years time in grade concerning 10 US Code 1370. I stumbled across this code a few weeks ago and sent it to the ‘Retirement Services’ section for clarification. I was told that my retirement would be based on highest grade held and current pay table. I was specifically told that “High 3″ does not apply to me. After a phone conversation, I was told that AR 135-180 applied (which I believe it does) and it says ” If the Soldier was transferred to the Retired Reserve or discharged on or after 25 February 1975, retired grade will be that grade which a commissioned officer or enlisted Soldier held while on active duty or in an active reserve status for at least 185 days or 6 calendar months. A warrant officer must have served on active duty or in an active Reserve status for at least 31 days”. There is no mention of 10 US Code 1370 in this regulation. This is not in alignment with 10 US Code 1370. I have since sent a request back to them asking them to confirm if 10 US Code 1370 applies or does not apply to me and I am awaiting a response. Who could answer this question definitively? The engineer in me needs to be given something definitive in writing.

Also, I was informed about the use of the “Value of a Point” table which seems to be the same, once converted, to the current military pay tables listed on DFAS/MyPay. Is that correct? Will my final “High-Three” be based on the military pay tables or “Value of a Point” table (which is I believe is the same thing) if I go into the Retired Reserve (grey area)?

Last question. My MRD is in 2029 however I will not turn 60 until 2034. Am I still authorized to stay in the Retired Reserve beyond my MRD to continue to get the pay increases toward my retirement at 60?

Thank you, in advance, for the feedback.

Mike

Doug Nordman says

Good question, Andrew, and the answer needs some math. I don’t use point valuation factors because they’re frequently approximated or even outdated. They also neglect additional expenses like health insurance.

Instead, I estimate the pensions at the different retirement dates and ranks.

From the information you’ve mentioned, it looks like you’ll turn 60 years of age in March 2021. (Please correct me if I’m wrong on that.) No matter when your pension may start, age 60 is when you’ll also be eligible for Tricare Prime or Select as a Guard retiree. That part is in federal law.

If you leave your drill billet before March 2021 then you’ll lose Tricare Reserve Select ($43/month or $218/month for member or family in 2019) and have to spend additional money for Tricare Retired Reserve ($452/month or $1083/month in 2019). You might find a cheaper health plan from a civilian employer or on the federal/state ACA exchanges but Tricare may have better copays, deductibles, and caps.

It also looks like you’re eligible to start your pension in November 2019. You’ll have to make sure that your 90-day periods are all done in the same fiscal year (up through September 2014) for deployments to combat zones. More details on those requirements are at Ryan Guina’s post:

https://themilitarywallet.com/national-guard-and-reserve-early-retirement-age/

More importantly, you’ll have to make sure that HRC agrees with your 90-day accounting and will start your pension in November 2019.

If you retire in the next few months then you’ll pay for your own health insurance for about 24 months. If you continue to drill until age 60 then you’ll receive drill pay (at the E-7 or E-8 rank) and you’ll keep Tricare Reserve Select. You’ll want to do the math for those incomes and expenses as well as your pension calculations.

You’re under a High Three pension plan, and your pension will be calculated from the average of the highest 36 months of pay. Those 36 months will probably be the ones just before your pension starts, and at the pay tables in effect when your pension starts. We already know the pay tables for 2019:

https://the-military-guide.com/2019-military-pay-chart/

but we don’t know the paytables for 2020 or 2021. You can estimate those future pay tables by hoping that military pay goes up 1.5% per year.

You’ll want to run three estimates, perhaps updated for your actual point counts:

1. Retire in March 2019 as an E-7>34 with 4046 points and start your pension in November 2019. You have to pay for health insurance through March 2021.

2. Retire in March 2021 as an E-7>36 with 4146 points (50 points per year) and start your pension immediately. You have two more years of E-7 drill pay and two more years of TRS health insurance.

3. Retire in March 2021 as an E-8>36 with 4146 points and start your pension immediately. You have two more years of E-8 drill pay and two more years of TRS health insurance.

E-7>34 or >36 pay in 2019 will be ~$5430/month, in 2018 is $5291.40/month, in 2017 was $5167.50/mo, and in 2016 was $5061.30. E-8>34 or >36 pay in 2019 will be ~$6197/month.

You could estimate that E-7 pay in 2020 tops out at $5511/month and in 2021 at $5594/month.

You could estimate that E-8 pay in 2020 tops out at $6290/month and in 2021 at $6384/month.

Now let’s calculate the pensions:

1. March 2019’s High Three E-7 average has nine months in 2016, 12 months in 2017 and 2018, and three months in 2019.

That’s [(9x$5061.30)+(12x$5167.50)+(12x$5291.40)+(3x$5430)]/36 = $5204.13

The pension is (4046/360) x 2.5% x $5204.13 = $1462/month.

2. March 2021’s High Three E-7 average has nine months in 2018, 12 months in 2019 and 2020, and three months in 2021.

That’s [(9x$5291.40)+(12x$5430)+(12x$5511)+(3x$5594)]/36 =$5436.02

The pension is (4146/360) x 2.5% x $5436.02 = $1565/month.

3. March 2021’s High Three E-8 average has nine months in 2018 as an E-7, three months in 2019 as an E-7, 9 months in 2019 as an E-8, 12 months in 2020, and three months in 2021.

That’s [(9x$5291.40)+(3x$5430)+(9x$6197)+(12x$6290)+(3x$6384)]/36 = $5953.27

The pension is (4146/360) x 2.5% x $5953.27 = $1714/month.

You can tinker with these formulas if you change the dates or the ranks. I hope this helps you figure out the best approach for your other considerations!

Andrew Kazensky says

Hi,

Can you help me figure out how the point valuation factor, used in retirement calculators, is determined? I want to decide if the increase in retired pay is sufficient to stay in the Air Guard as a Drill Status Guardsman (DSG) another 28 months, until I reach age 60, or if I should just retire in the next few months. Additionally, I would like to know the increase of retired pay if I could get promoted to E-8 in the next 4 months (need 24 months retainability to be promoted). To do this, I am using the Reserve Retired Pay Calculator (https://mypers.af.mil/app/processes/form/fn/rpc). However, I cannot figure out how to determine the point value to use in the calculator for the “Member Projected Information” section when using the “Future Pts Value” selection of the “Based on Pay Table of Year” required information.

I have 4,046 points as of today which equates to 11.239 years of service, and that equates to a .281 pay multiplier.

My LES shows 34 years of service so I am over 26 years for pay purposes. Therefore, the 2018 E-7 monthly pay for over 34 years/26 years is $5,291.40, and $5,291.40 * .281 = $1,486.74 That is pretty good for doing what I love..serving my country. But, I am beginning to feel the time is near for retirement. So, is there a financial advantage to going to age 60, 28 more months, as an E-7? Is there an advantage to trying to get promoted to E-8 and then go to age 60? I am eligible for reduced retired pay in Nov 2019 due to active duty performed after January 2008.

Thank you.

Doug Nordman says

Good questions, Harry.

DFAS calculates a pension using the DoD Financial Management Regulation (DoD 7000.14-R) volume 7B chapter 3.

https://comptroller.defense.gov/Portals/45/documents/fmr/current/07b/07b_03.pdf

You’d follow along in paragraphs 030201, 030203, 030205, and 030208, and 030209. Maybe you’re also covered under 030204.

First, you’d want to make sure that you’re indeed eligible for Final Pay (a Date of Initial Entry on Military Service on or before 8 September 1980). 33 years implies that you joined in 1984 (High Three) but you may have joined earlier and had some interrupted service. More importantly, you want to make sure that DFAS also has that information in your record, or else they’ll default to High Three.

Next, verify that you and DFAS are using the same point count (3837 points?). If they’re using a different number then you’d have to correct that with your drill records and your DD-214s.

Third, what year did you start your retirement? For the vast majority of Reserve & Guard retirees eligible for Final Pay, it’s your 60th birthday year. If your Reserve pension starts at age 60 and your 60th birthday was in 2017, then you base your pension on the 2017 pay tables. If your 60th birthday is in 2018 then you start with the 2018 pay tables. (A few Reserve/Guard members deployed for at least 90 days in a fiscal year to a combat zone or for a national emergency, and they’d start their pension at least three months sooner. More info on that is at:

https://themilitarywallet.com/national-guard-and-reserve-early-retirement-age/ ) You’re also right that you start with the years of longevity as though you’d been on active duty all the way up to the start of your pension. At the E-7 paygrade, that tops out at E-7>26.

Finally, the Final Pay formula is

(Points / 360) x 2.5% x base pay = $/month

According to the rules in the FMR, the first division is carried to three places and rounded to two. The formula’s resulting dollar figure is rounded down.

If you started your pension (60th birthday) in 2017 then your deposit would be

(3837 / 360) x .025 x $5167.50 = 10.66 x .025 x $5167.50 = $1377/month.

If you started your pension in 2018 then your deposit would be

(3837 / 360) x .025 x $5291.40 = 10.66 x .025 x $5291.40 = $1410/month.

Let me know if I’ve made any incorrect assumptions.

Harry Horner says

Good Morning to all, let me start off with my retirement has been a pain since Dec 2017, after 33 years active and reserve I have learned to dot my i’s cross my t’s because all forms had to be correct,and what not,well I guess my problem is with DFAS seems to me after phone calls emails letters etc, they pretty much do what they want? One good conversation with a gentleman there actually to me to send a copy of my orders to them and they will correct them, enough said. So since December my retirement has not been correct period. I have used the calculators formulas etc, and what I have doesn’t match what DFAS has? So, what does a retired E-7 over 26 years (final Pay) option with 3837 points supposed to receive (gross) 3837~360=10.6583333333×2.5%=0.2664583333×5291.47=1409.9562770833 if I am supposed to use the current 2018 pay scale for E-7 over 26 if I can get corrected on this or I’m on the right path please let me know, Thanks

Doug Nordman says

Good questions, Peter, and your retired rank is indeed based on your highest grade earned. Here’s the federal law:

https://www.law.cornell.edu/uscode/text/10/3963

Keep in mind that the NC Army NG and Army HRC have to have your Navy records on file. You already have your Notice Of Eligibility and your approval for retired awaiting pay, but you should verify with Army HRC that they also have your record of satisfactory service as an E-7.

My apologies if you already know this, but hang on to your records until your pension starts. You may have to “prove” it to HRC one more time when they contact you (around age 59.5) to do the final paperwork for your pension.

You retired awaiting pay in 2007 as a NG E-7 with 21 years of service, and your longevity advances (until your pension starts) just as if you were on active duty the entire time. By 2018 you’re an E-7>32 years whose base pay is $5291.40. Pay raises are typically 1.5%-2% per year, so a conservative High Three average of the three years of pay tables in effect when you turn age 60 would be about 96% of the latest base pay.

In today’s dollars your pension would be roughly:

(5100 points / 360) x 2.5%/year x ($5291.40/month x 96%) = $1800/month.

Peter M. Heiman says

Doug,

I am very appreciative of the information that has been presented here as it has answered a number of questions I had. If I could bother you for an analysis of my situation I would greatly appreciate your feedback.

I spent 11 years (1983 – 1994) in the active US Navy where I achieved the rank of CPO (E-7). My discharge DD-214 shows E-7 as my discharge grade, my discharge was R-1 Honorable. I was out of the service for 3 years. I returned to service in the North Carolina Army National Guard at the rank of E-6. I was told that upon reaching retirement age (60) my pay would be based on E-7 as this was my highest rank attained. I remained an E-6 throughout my 10 (1997 – 2007) years in the NCANG and retired at this grade. I have my “20 year letter” and I have a little over 5100 points with the active Navy, reserve time and an activation in 2005 – 2006. I elected to “retire awaiting pay” as I saw that the financial upside was worth the possibility of being re-called.

I have a few questions: First, where they correct in saying that my retirement pay would be based on my highest grade earned?

Second, if above is correct, when and how do I make that change?

Third, based on the info I have give and your knowledge, what is a ballpark figure for my retirement? I understand I am high three so current pay scales would be great for now.

Thanks!

Doug Nordman says

You’re right, Keith, Reserve & Guard servicemembers have a lot of edge cases in a very complicated pension system.