Before I joined the Air National Guard last year, I decided to transfer the funds from my Thrift Savings Plan account into an IRA. There are many pros and cons for deciding to transfer your funds to an IRA, so this is something you should look at from all angles before deciding to make the decision. A Thrift Savings Plan Rollover into an IRA can also be complicated, so get help from an investment professional if needed.

To start with, the TSP is actually one of the best retirement plans available due to the low expense ratios for the funds. I had previously kept my funds in the TSP because it gave me the option of transferring other IRAs or retirement funds into the TSP account at a later date. But as I was going to join the Air National Guard, it didn’t matter if I closed out my old account, since I could open a new TSP account once I joined the ANG.

The other reason I transferred my funds out of the TSP was to move my tax-exempt contributions out of the TSP and into a Roth IRA. The tax-exempt contributions were held in a Traditional TSP, and were made while I was deployed to a tax-free zone. Since those contributions were made with tax-free pay, they are eligible to be transferred into a Roth IRA – this has huge long-term tax benefits (see below for more information). But I had to liquidate the entire TSP account to access those funds.

First Step – Decide if Closing Your TSP Is Right for You

As I mentioned above, the TSP is a great retirement account due to the low expense ratios. There are also no added expenses or fees for keeping your Thrift Savings Account open, so if you don’t have a specific reason to close your account, you are probably better off leaving your TSP account open. Low fees and flexibility are important in investing.

Additionally, you are able to transfer external funds into your TSP account from other retirement plans, including 401k plans, other TSP accounts, IRAs, and similar plans. You just won’t be able to make new contributions if you are no longer serving in the military or working for the federal government. So keeping your TSP account open can be a good thing if you want to take advantage of the low expense ratios.

Here are some articles to help you make the decision:

- What to Do with Your TSP When You Leave the Government or Military Service.

- Should You Rollover Your TSP into an IRA?

As I mentioned above, in most cases, it makes sense to leave your account open unless you have a specific reason for moving the funds out.

You Decided to Roll Your Thrift Savings Plan into an IRA… Now What?

Once you make the decision to transfer your funds, you need to make sure you do everything in the right order to make sure the transfer or rollover goes smoothly*. Otherwise, you may find it takes too long to complete the transaction. This is important because the IRS could classify the transaction as a withdrawal if you don’t make the deposits quickly enough. This can include early withdrawal penalties (if under age 59.5), and paying taxes on the withdrawal amount. So be sure the enlist assistance if needed.

*Terminology note: The terms “Transfer” and “Rollover” are sometimes used interchangeably with retirement accounts. Transferring an account means the funds are transferred directly from one financial institution to another. A Rollover happens when the funds are sent to the investor, and the investor needs to deposit them into another qualified retirement account within a certain time frame, and according to IRS rules. This is important because it can have major tax implications if not done correctly.

Open an IRA Before You Start Any Other Paperwork

You need to open an IRA before you can transfer the funds from your TSP. You can request the Thrift Savings Plan write the check out to you, but it’s much faster and easier to directly transfer the funds to an IRA that has already been opened. This also reduces the likelihood of running into issues with the IRS.

You will need provide your bank or brokerage account and IRA account number when you make the funds transfer. If you already have an IRA, you can simply transfer the funds into your current account. If not, you will need to open a new IRA. Start by researching financial companies. We have a list of recommendations here, or you can go with any of the major military financial institutions (USAA, NFCU, PenFed) or major brokerage houses (Vanguard, Fidelity, Charles Schwaab, TD Ameritrade, etc.).

Make sure you have both a Traditional IRA and a Roth IRA if you have funds in both the Traditional and Roth sections of the Thrift Savings Plan, or if you want to send your tax-exempt contributions to a Roth IRA (see below for more information about this process).

Complete the Required TSP Paperwork

The next step is to start the paperwork from the Thrift Savings Plan. You can transfer some, or all, of your funds into an IRA. In fact, if you want to liquidate the majority of your TSP funds, but keep your account open, then leave at least $200 in your account, which is the minimum to remain open. You then maintain the flexibility of transferring funds into the account at a later date.

To make transfers or withdrawals you will need to download and fill out the required form:

- Form TSP-70 Request for Full Withdrawal (PDF)

- Form TSP-77 Request for Partial Withdrawal When Separated (PDF)

Then you need to complete the required sections.

Filling Out Form TSP-70 Request for Full Withdrawal. If you are doing a full withdrawal (transfer or rollover of the entire contents of your TSP), then you will need to fill out pages 1, 2, and 4 (Traditional Balance) and/or Page 5 (Roth Balance).

- Page 1 includes your personal information, and personal information for your spouse, if you are married. You will need to get your spouse to sign off on the transfer and get the signature notarized. This is a security feature to make sure both parties agree with the transfer. Many banks provide free notary services to members. Otherwise check your phone book or the Internet to find a notary public.

- In page 2, section 4, you declare how you want to take the withdrawal – as a single payment, life annuity, or monthly payments from the TSP. If you are transferring to an IRA, choose 100% for the Single Payment option. Of course, you can split this among different options if you choose. Select the Check Box in Section V to indicate you are transferring your assets to another retirement account. Section VII on page 2 requires your notarized signature to authorize the transfer.

- Finally, on Page 4 and Page 5 you indicate where you want the funds to be sent. You will need to include the address of your IRA custodian and the account number where you want the funds to be sent. You will then need your financial institution to fill out the remainder of page 4* or 5 (a verifying official needs to sign the form before the TSP will process it). Then your IRA custodian will fax or mail the completed form to the TSP.

- *See instructions below if you have tax-exempt contributions – this is important because your IRA custodian fills out this section. Instructions below.

- The Thrift Savings Plan will send a check directly to your custodian (for benefit of your account), and it should be deposited into your IRA.

Filling Out Form TSP-77 Request for Partial Withdrawal When Separated. This process is very similar to the above process, but the page numbers and sections numbers are different. Read through the directions very carefully to make sure you don’t miss anything. If you have questions, call your IRA custodian to walk you through the form. Even if they don’t transfer a lot of TSPs, they should be able to understand everything enough to be able to help you out. If they don’t, then look around for an IRA custodian with better customer service.

Transfer Traditional Funds to a Traditional IRA, Roth to a Roth IRA

It sounds basic, but you want to get this right the first time. When you are transferring your TSP funds, make sure you transfer them to the correct type of account. This will prevent problems with the IRS. Both the TSP-70 and TSP-77 have sections for both Traditional and Roth contributions and transfers.

If you want to convert a Traditional account to a Roth account, it’s best to do this in two separate transactions. Complete your TSP to IRA Rollover, then perform a Traditional IRA to Roth IRA rollover.

Be Careful with Tax-Exempt Contributions!

If you participated in the Traditional TSP when you were in a tax-free location, you most likely have tax-exempt contributions (this does not apply to the Roth TSP; it only applies to funds in your Traditional TSP account). To verify you have tax-exempt contributions, you should see something like this on your TSP statement:

You DO NOT want to transfer these funds into a Traditional IRA. These contributions are tax-exempt, so you are eligible to roll them into a Roth IRA. The long-term benefits of this are huge. Here is the difference:

- Contributions to Traditional IRAs, 401k plans and the TSP are considered pre-tax contributions, meaning you make the contribution before your income is taxed. This lowers your taxable income in the tax year you make the contribution. The funds then grow without taxes until you reach retirement age. The money is only taxed once you begin making withdrawals.

- Roth IRAs are the opposite. They are considered post-tax contributions. The funds are contributed after you have paid your taxes, then they grow tax free until you take withdraw the funds. You will never pay taxes on those funds again. The law allows military members to contribute tax-free income to a Roth IRA, meaning you will never have to pay taxes on that money – either the contributions, or the earnings.

In other words, the funds you transfer into a Traditional IRA will be taxed when you make withdrawals in retirement, but anything transferred into a Roth IRA will never be taxed again. Transferring the tax-exempt contributions into a Roth IRA gives you years of compounding growth without ever having to pay taxes on any of the gains. This is HUGE.

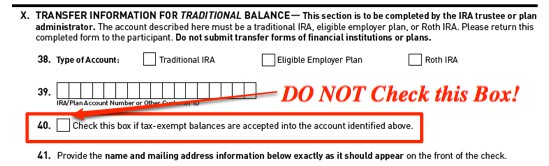

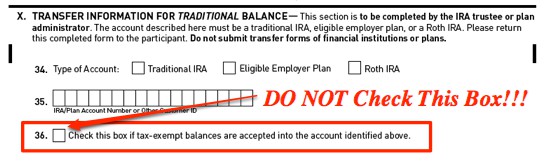

How to Transfer Your Tax-Exempt Contributions Correctly

You can prevent your tax-exempt funds from being transferred into a Traditional IRA by NOT selecting the following Boxes in the forms:

Form TSP-70, Section X, Box 40. Do NOT Check this box!

Form TSP-77, Section X, Box 36. Do NOT Check this box!

Note: Section X is also the section that your IRA custodian fills out certifying you have an open account with them. When I transferred my TSP funds into an IRA, I sent a cover letter to my IRA custodian explaining my wish not to check Box 40 on Form TSP-70. I strongly suggest including written documentation to your custodian to ensure they do not check this box!

Tax-Exempt Funds are Sent to You as a Check – Be Careful with This! By not checking the box above, you are telling the Thrift Savings Plan that your custodian cannot accept tax-exempt contributions into your account. Thus, the TSP will disburse those funds in a check made out to you. This money is non-taxable, so technically, you can do anything you want with it, including cashing it and spending it. But that would be a long-term mistake since you can roll it directly into a Roth IRA and earn tax-free growth on your investments.

Once you receive the check, you will need to send it to your IRA custodian with instructions that it should be deposited into a Roth IRA. When I sent in my check, I signed the back and wrote the IRA account number on the back. I also included a letter stating that it was a Rollover from the Thrift Savings Plan. This is important information for the financial institution to note so they can code it correctly for the IRS. Failure to give them this information can cause problems down the road.

Understand the Tax Implications of Your Transfer

In most cases, there won’t be any issues if you transfer your funds directly from a Traditional TSP to a Traditional IRA, or from the Roth TSP into a Roth IRA. In both cases, the Thrift Savings Plan will issue you an IRS Form 1099-R at the end of the year (a 1099-R is issued for Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc., pdf). This informs the IRS there was a distribution from your retirement account.

The company that receives the IRA will issue you an IRS Form 5498 (IRA Contribution Information, pdf). This is a tax form that shows the funds were deposited into another retirement account. These forms will prevent you from getting tagged with an early withdrawal penalty, taxes, or other nasty surprises.

If you do a Rollover, and not a Transfer, then you need to make sure the gaining institution codes the contributions correctly so you can avoid any problems with the IRS. You will still receive the IRS Form 5498 if you manually rollover your funds into an IRA vs. doing a direct transfer. Make sure to get some form of confirmation letter from your financial institution stating they received the funds and they were deposited into your IRA.

How Long Does a Transfer / Rollover Take?

As you might guess, this is variable, depending on how busy your IRA custodian is, how long it takes the TSP to process your paperwork, etc. That said, I’ve personally transferred two TSP accounts (one for myself, and one for my wife) and both were completed in less than 2 weeks. But it can take up to a month in some cases.

Obligatory Disclaimer: There are many factors to consider when transferring retirement accounts. Be sure you consider possible impacts on your tax situation, future retirement planning, etc. You may wish to consult a professional for more personalized and specific advice and recommendations.

Comments:

About the comments on this site:

These responses are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser’s responsibility to ensure all posts and/or questions are answered.

:uke says

Ryan, I know this article was posted some time ago. While I am still dealing with the shock of realizing that the growth on my tax-exempt contributions is actually -not- tax-exempt (despite a pie chart and table on the new TSP site saying it is), it would seem like things have gotten easier with the paperwork (but this is a question more than a statement).

As I go through the online instructions, it seems that I -would- check the box that my current employer accepts tax-exempt balances. It then asks you to which accounts do you want to send the tax-exempt balance (really the tax exempt contribution) and where you want to send the taxable balance.

My plan would be to transfer the tax exempt balance directly into my Roth IRA and the taxable balance into my qualified 401K plan with my current employer. (both managed by the same institution). No check to me. Just that tax exempt balance from my traditional TSP account directly into the Roth. You said a few times that you can contribute your tax-exempt amount directly into a Roth but then it sounded like you were saying you can’t do that. Just trying to get some clarification there. Thanks.

Steve Hopwood says

I hate TSP. A million different ways to contribute, but ABSOLUTELY ZERO ways to get your money out. TSP form 70? where is it located? Not on the TSP website. And why should I have to pay for the forms from a private website?

Jennifer Ludders says

This article was so helpful! Thank you so much. Now that 3 years have passed I will need to make sure all the info is still current (according to one commenter it is not), but this is an incredible useful place to jump off from.

King Cooley says

Staff:

Recently, I viewed a text from the TSP board requesting me to call your office regarding my transfer from the TSP investment on my job to an IRA. Before I was able to return the call, somehow the message had dropped out of the phone. my phone is defective having been dropped many times. Can you give me the contacts with the TSP section that wishes to contact me concerning my Rollover from the Civilian TSP to an IRA. I believe there was a mention of consent.

Ryan Guina says

Hello King,

I recommend contacting the Thrift Savings Plan ThriftLine at 1-877-968-3778 or use the Message Center through the “My Account” section of the TSP website.

Best wishes.

Rob R says

You will want to update the above referenced article, since it is out of date. Sometime after 2018, TSP terminated its TSP Form 70 & 77 process and now transfers must be done via its “Making an in-service withdrawal” TSP-75 (Web) form process (see https://www.tsp.gov/in-service-withdrawal-basics/making-an-in-service-withdrawal/).

According to the referenced TSP webpage the transfer is via US Postal Service Mail, NOT electronic transfer.

“If you are transferring your age-based withdrawal to your IRA or eligible employer plan, we’ll mail the check to your IRA or plan.

You should expect that it will take up to 10 business days from the time we receive your properly completed request until the time we send your check.”

I am at day 25 awaiting the check. According to the TSP helpline the mailed check was sent without a tracking #.

Jeremy says

Just a heads up your TSP info is out of date.

PSH says

I can’t figure out how the TSP sends monthly transfers to an IRA.

I see how I make the request, but do they mail monthly checks to my brokerage or do they transfer the funds electronically?

Don says

Hi Ryan,

I transferred to another agency within the federal government civil service and want to know if I can transfer money from the first federal agency into a independent IRA plan. While I stated a civil servant, I changed agencies. There was no break in service.

Ryan Guina says

Hello Don, If you didn’t have a break in service, then I believe your funds are required to remain in the TSP. I don’t believe you can do a rollover while you are still employed by the federal government. You can contact the TSP customer service desk to verify. Best wishes!

Jason says

Hello Ryan,

Thanks for the brilliant article. I’m a bit confused on the limitations of TSP transfers and thought you might provide some insight. I’ve been in the federal service for some years now and I’d like to transfer my TSP traditional to an IRA tradition to give me greater control with my investing. I haven’t reached 59 1/2 (I’m 45) and so many articles indicate that this as the magic age. Is there any opportunity to transfer a portion of my TSP to an IRA if I’m still employed by the govt? How much a penalty should I expect to pay if I’m intent on making the transfer and would I be permitted to do so without penalty if I landed a job in the private sector? Many Thanks

Ryan Guina says

Hello Jason,

You cannot transfer your TSP to an IRA if you are still employed by the government (or military). However, you can transfer your TSP to an IRA once your employment stops.

There is no charge from the TSP to transfer your funds to an IRA, and investment companies shouldn’t charge you anything either. There shouldn’t be any tax consequences either, provided you transfer directly from a Traditional TSP to a Traditional IRA.

Be sure to have the TSP send the funds directly to your new investment company if at all possible, this eliminates the risk of not transferring the funds in time. You may have to pay IRS penalties or interest if you receive a check from the TSP and take too long to deposit the funds into a new qualified investment account.

The age 59.5 is the magic number for being able to make withdrawals from your TSP without penalty, though you would still have to pay taxes on any withdrawals from a Traditional account, since the funds were deposited before taxes.

The age 59.5 doesn’t come into play if you are transferring your TSP to an IRA, qualified annuity, 401k, 403b, or similarly qualified retirement account.

I hope this is helpful!

Suzanne says

Oh my goodness what a great article. Thank you for keeping up with the comments years later. I just got off the phone with someone at TSP about rolling over my TSP to an external plan after leaving federal service and they said they don’t have a list of the type of plans I can roll it into without penalty, lol. They said it has to be a company’s retirement plan, an SEP, an annuity plan, etc. (401A, 403A,B,C, etc.) They didn’t think I can roll it into an IRA.

Will I pay a penalty for rolling it into an IRA or Roth IRA?

If so what is the penalty? Local, state, federal taxes or a fee per $?

They recommended I fill out form TSP-99 not the TSP-70 or TSP-77. So confused. Any insight would be greatly appreciated!

Ryan Guina says

Hello Suzanne,

My pleasure. You will not pay a penalty for rolling your TSP into a qualified retirement plan, which includes the plans you mentioned, as well as an IRA.

That said, you want to make sure you roll Traditional TSP funds into a Traditional IRA, and a Roth TSP funds into a Roth IRA. This ensures the funds retain the same tax classification.

You can later convert the Traditional IRA to a Roth IRA if you wish to do so, but you would have to pay taxes on the amount of the conversion (since Traditional IRA funds are made on a pre-tax basis and have not yet been taxed).

In the case of tax-exempt contributions, you can roll those into a Roth IRA, since those contributions were never taxed in the first place.

It may be a good idea to speak with a tax planner or financial planner to ensure you do things properly, as making a mistake on the conversion process could be costly. A financial planner can also help you choose the correct form to use.

Best wishes!

Roshan Jagsi says

Does transferring TSP pretax money to Traditional IRA mean no more RMD?

Ryan Guina says

Hello Roshan,

No, you will still have to do RMDs with a Traditional IRA. However, there is no taxable event for rolling your TSP funds into an IRA. So you can move the money into your IRA if you prefer to do so to take advantage of other investment opportunities or to simplify your investment management.

On the same note, you can transfer your IRA into the TSP if you prefer to manage everything through the TSP (again, to take advantage of the investment options in the TSP, maintain low costs, and to simplify management). Here is more information.

Either way, you will have to make Required Minimum Distributions to the IRS.

I hope this is helpful.

Dave says

Great article.

I’m currently in a term fed position that will end next year. In my uniformed services TSP, I have $16K in tax exempt contributions and $8K in earnings on those tax exempt contributions. I also have a civilian TSP account with about $300K. When I leave federal service, I want to move it all to my Vanguard IRAs. Do I have to fill out separate TSP forms to move 1. the tax exempt contributions 2. earnings from the tax exempt contributions, and 3. the civilian contributions and earnings?

Basically, I’d like to rollover tax exempt TSP contributions into the Roth IRA and the earnings from the tax exempt TSP contributions to a traditional IRA along with the civilian traditional TSP so I can begin a Roth conversion ladder

John says

Ryan,

I am a full time technician in the National Guard and recently converted to an AGR position. I understand that I am under USERRA rights but plan to keep my AGR as career. I would like to transfer my TSP that I have built up on the technician side to another IRA (w/out taxes or penalties) but was informed I would need to separate to be eligible to transfer. Since I can’t contribute, with matching, on the civilian TSP I find it difficult to leave it stagnant there when it could be creating investments in another IRA. Would you have any information on transferring it out to another IRA?

Ryan Guina says

Hello John,

This is a great question. I’m not sure what the process is for rolling your funds out of the TSP if you have reinstatement rights to your Civil Service job. I would contact the TSP or your HR department about this. They should be able to let you know how to do this, or if you would have to give up your reinstatement rights in order to transfer out the TSP funds.

Regarding leaving the money in the TSP vs. an IRA: there is no right or wrong here. Your money can still grow in the TSP even if you can no longer make new contributions. You can make your future contributions to the military TSP or you can open an IRA separately and make contributions to that each year. You aren’t missing out by leaving your funds in the TSP.

That said, I can understand the desire to roll your TSP funds out of the TSP if you want to consolidate accounts or if you want to invest in a fund or another investment you don’t have access to through the TSP.

I hope this points you in the right direction. I wish you the best, and thank you for your service!

Robert Vittetoe says

I sure would have liked to have had this information in 2008. I transferred about 28k from my TSP that were tax exempt contributions and about 30k in pre tax contributions. In 2008 USAA recommended putting the tax exempt and pre tax in separate accounts both were traditional IRA accounts. Reading your article the tax exempt could have gone into a Roth. Now USAA won’t make a recommendation. They suggested I see a tax advisor to determine if the tax exempt money and the 11 years of growth can be converted over to Roth without any costs or penalties.

Carina says

I am 63 year old female retired from federal service after 10 years, I have money in my Traditional TSP and wanted to know if it would be beneficial to start rolling it over to IRA now, then gives me 7 years to roll it into Roth IRA for tax free money at retirement. Would you advise that I do that now, I have $180,000 TSP? Please advise! Thank you!

Rosie Duran says

how do I request to roll over to my former spouse’s IRA account the portion of contributions made while our marriage? is there a form we must complete? we already have the marital settlement agreement and judgment submitted

Alvin R says

Minimum to keep a TSP account open is $200 not $500 as Summary to Thrift Savings Plan PDF, page 19

Ryan Guina says

Thank you, Alvin. This has been updated. I appreciate it!

Daniel Deiler says

Ryan,

Correct me if I am wrong, but it sounds like taxes are paid on non-tax exempt funds when rolled over from a traditional to a ROTH fund at the end of the year when taxes are filed and NOT at the time of the transfer (which to me sounds like it makes a heck of a lot more sense to do it that way instead of having to wait til taxes are filed. It could be treated JUST like a paycheck and taxed at the same rate you have designated on your W-2’s.

Ryan Guina says

Hello Daniel,

Thank you for your comment.

I believe you have the option to have taxes withheld from your rollover. However, that is generally the least effective long-term option because it reduces the amount of money you are rolling into a Roth fund. It’s better to pay the taxes out of pocket if you are able. This gives you more money in your Roth investment, which will grow tax free until retirement.

Having taxes withheld would be easier, but more costly in the long run. If the taxes on the rollover are too much to handle the entire amount at once, then it may make sense to roll the funds into a Roth account over a several year period. This is a strategy often used to limit the tax bill in any given year, as well as avoid going too deep into a higher tax bracket on the transferred funds.

There are many ways to do a rollover, and each situation should be viewed based on individual circumstances. I strongly recommend speaking with a tax professional or investment advisor about your options and the best path going forward.

I hope this is helpful. I wish you the best, and thank you for your service!

Dean Yoder says

What’s the percentage of tax do I pay when I rollover from a traditional TSP account to a Roth IRA?

Ryan Guina says

Hello Dean, Thank you for contacting me. You will pay your Federal Income Tax rate, plus your state income tax rate. Some people only roll over a portion of their Traditional IRA each year so they can minimize the tax impact.

For example, you can project your income from all sources for the year and rollover an amount that will take you close to the tax bracket you are already in. Then repeat the process the following year. This can help avoid going to far into higher tax brackets.

This can be a complicated topic, depending on your situation. So it may be helpful to consult with a tax professional or financial planner to ensure you are doing this in a tax efficient manner. I wish you the best, and thank you for your service!

Nancy Wingo says

my husband turns 70 1/2 …he is having memory problems…I am trying to find out if he has to just take the money out of his TSP or if he can “rollover’ that money into some other investment and avoid paying all those taxes. I don’t want him making a financial mistake…and I am so ignorant on the whole subject. please help direct me somewhere. nancy

Raquel says

Is it possible to do a partial transfer (leaving the $200 as you explained in your post to keep a TSP account) and transfer all your tax-exempt funds into a Roth IRA? Or do you have to close/pull ALL funds to be able to do that?

If my husband will not have access to a TSP again as you did, which is better, Having an accessible TSP account or transferring (the small amount of) $450 of tax-exempt funds to a Roth IRA?

Jeff says

Ryan,

Have you heard of anyone’s IRA custodian refusing to leave box 40 on the TSP-70 form unchecked? I had that happen to me with two different brokerages where I have IRAs (Ameritrade and Fidelity). I haven’t given up just yet though. I plan to call TSP again. I may give USAA a call since I see that is who you used. There has to be a way to get my tax exempt money out so it isn’t rolled into the traditional IRA. Still trying.

Ryan Guina says

Hello Jeff, Thank you for your question. I only have the personal experience I noted in this guide. This is not a common situation, so it’s worth using an investment firm that has experience processing these transfers – just to make sure nothing gets messed up in the process. I called USAA and had their customer service reps walk me through the process while I was on the phone. It’s too important to mess this up, as the Roth characterization will have a massive long-term impact on your investment portfolio.

If you decide to use USAA, you can always transfer that IRA to another firm later, if you decide to do so. The most important thing at this point is to get the transfer done correctly so your tax-exempt contributions can be put into a Roth IRA. You can always change the asset allocation or IRA custodian at a later date.

I wish you the best, and thank you for your service!

Jake says

Ryan,

You mentioned that you transferred your TSP into an IRA prior to joining the guard. Did this not net you early withdrawal penalties? If I were to complete my enlistment and then turn my tsp into a Roth ira, would I be dealing with these early withdrawal fees or just paying taxes on the amount? Also, if I were to go guard without swapping over my account, would I be able to contribute to my preexisting tsp account or would I need to have a new one? Does being employed by the guard prevent me from withdrawing or transferring money the same way active duty does?

Brian says

Ryan,

Is there any specific reason for transferring a traditional balance to a traditional IRA prior to rolling it into a Roth IRA? To me, that seems like a needlessly paperwork intensive step since I’m fairly certain I can simply have it all transferred to the Roth IRA directly. I completely understand the tax consequences of this and luckily I’m in a low tax bracket this year to make this worthwhile, but besides that issue I can’t see any other issue. I do have a small amount of tax-exempt money, but I don’t think that should create an issue since it’s going directly into a Roth and shouldn’t pose any tax issues as long as it is coded correctly. I’d appreciate your input. Thanks.

Ryan Guina says

Hello Brian, Thank you for contacting me. I don’t know if there is any issue of making the transfer directly to a Roth IRA. I have always made the transfer into a Traditional IRA first so there was a clear paper trail. I believe I did this a the recommendation of the company I transferred my TSP into (USAA). I requested the tax exempt portion be made out to me the form of a check, which I then immediately deposited into a Roth IRA.

I don’t want to make a definitive statement either way, since I’m not sure if there is any issue with making a direct rollover into a Roth IRA. I would ask the company that you are rolling the TSP into and go with their recommendation. In many cases they will also help you with the paperwork. Sorry I don’t have a better answer. Best of luck with your transfer, and thank you for your service!

Bob Widmaier says

Hello Ryan,

I want to directly transfer my Traditional TSP account to a Traditional IRA. Page 2 of the TSP 79 for the transfer is labeled as optional. What are the chances that the TSP processing will misplace this page 2 and / or make a mistake and not directly transfer the account – but rather send me a check which would have very bad tax consequences and tax witholding? Is there anything I can do to help prevent errors other than my getting the TSP 79 page 1 and 2 filled out correctly and checked by the call center? Is there any advantage to having the other (large) institution file fax the TSP 79 and pull the funds?

Ryan Guina says

Hello Bob, Thank you for your question. I had my gaining financial institution file the form with the TSP and the transfer was handled with no issues. The organization I used had a lot of experience working with the TSP (many do), so I felt more comfortable going that route. They should be familiar with the process (it’s the same as transferring any retirement account, such as a 401k, 403b, 457, etc.). It also shouldn’t be a huge deal if the TSP sends you a check, provided you deposit it into a qualified retirement account (such as your IRA or another 401k-style account) within the specified time frame. If you have doubts, then it may be a good idea to have your gaining financial institution handle the transaction. Speaking with customer service should also help alleviate any concerns you may have. I hope this helps. Best of luck, and thank you for your service!

Jose says

Ryan, thank you for the time and effort in making this article for us! That being said, I am a new soldier in the National Guard, and so I was not familiar with TSP. I hope you will consider some of the following questions: Are you limited using your drill pay to make contributions to the TSP? If you can contribute civilian pay to your TSP through the National Guard, what are the rules on matching contributions? Again, I thank you very much, sir, for your time!

Ryan Guina says

Hello Jose, Thank you for contacting me. You can only make TSP contributions from your military pay. You cannot contribute outside money into your TSP. So you are limited to using your Drill Pay, pay from AT Days, or pay when you are activated for training, mobilizations, etc.

The Thrift Savings Plan and civilian 401k plans have the same contribution limit ($18,500 in 2016). You can’t exceed this limit. So if you contribute $15,000 to a civilian 401k plan, the most you would be able to contribute to the TSP would be $3,500.

There are no TSP matching contributions at this time, though the new military retirement plan will begin offering matching contributions starting in 2018. To participate in matching contributions, you would need to change your retirement plan. It will be a good idea to run the numbers before making any changes, as there are some long-term implications of changing retirement plans.

Mark H says

This got me thinking, but to be clear you can’t do an in-service withdrawal from the TSP, correct? (i.e. I will need to wait until retiring from the Reserves to take a withdrawal in order to get the non-taxable combat pay into a Roth IRA). Thanks

Ryan Guina says

Mark, Thank you for contacting me. That is correct, you cannot do an in-service withdrawal to transfer your funds to an IRA. You will have to wait until you are no longer eligible to contribute to the TSP to be able to transfer the assets to an IRA – this goes for both military members and those in the civil service.

Also note this only applies to the specific TSP account. For example, if you are in the Guard or Reserves and you have a military TSP, and you are also civil service and you have a government TSP, you can only transfer funds out when you are no longer eligible to contribute to that specific account. An example would be a Guard/Reserve member who retires from the Guard/Reserves, but continues the civilian job. They could transfer the military TSP into an IRA (or any other retirement account), but they would have to leave their civil service TSP open.

In your situation, you will have to wait until you are no longer eligible to contribute to the military TSP. Then you can consider doing the transfer or rollover. And that may be worth looking into if you have a lot of tax-exempt contributions. I hope this helps!

Mike d says

Transfers are allowed if you are over59-1/2.